Venture Deployment - could it be a thing?

A new asset class needed for the energy transition

I think about this a lot at CFS - where will the capital come from for the first few ARCs (our commercial fusion power plants)? There are other climate tech startups that I admire that likely are asking the same questions: Where and who are the capital providers that will invest in the early deployments of fusion, green steel and green cement plants, novel carbon free chemical plants, industrial scale alternative protein plants, industrial scale green hydrogen, the sustainable mining projects for lithium, cobalt, copper, iron ore …you get the idea.

As a systems thinker, and as an entrepreneur working to find the next capital, this feels like a problem in the industry. Sure, in the absence of the industry self-organizing to support this problem, there will be companies and projects that get funded, and those who will power through and force their way to a solution. But I can’t help thinking that this is not efficient, does not help the world meet our climate goals, and is also a massive untapped opportunity.

When you think about the level of innovation that needs to get developed and deployed, and the role that it will play globally in truly decarbonizing, it has led me to the conclusion that it feels like there needs to be an entirely new asset class. An entirely new type of capital that is purpose built for this. It can’t be a one-off fund, but needs to be a fund structure or capital structure that is replicable and scalable. Because ultimately this will be a global thing. Maybe it should be called “Venture Deployment.”

The Problem

If you spend enough time in the climate tech space, inevitably in your journey you start learning about the “valley of death” of financing the first-of-a-kind deployment (FOAK) gap. There is lots of good discussion of the problem, and an increasing amount of attention, synthesis, and understanding to it. Prime Coalition has the most comprehensive report I’ve seen on the topic. Forbes featured an article written by Rob Day of Springlane Capital. Albert Wenger of USV recently posted about the shape of the problem as well. Deanna Zhang highlighted the problem and proposed one novel approach. And I was extra pumped to see CTVC do a great dive into this just last week.

The quick summary of the problem is:

Typically, infrastructure projects are invested in by project finance - an off-balance sheet financing arrangement that is a combination of equity and debt, and depends on project’s long term projected cash flows for repayment.

These are complex sets of transactions, but are structured in a way to optimize the cost of capital to the project, and enables the company(ies) involved in the projects to rapidly scale and to do so more profitably. It is also ideally more effective in assigning risk to those best able to understand and mitigate it.

However, this type of capital is not positioned or willing to invest in projects that are based on new technology that is being scaled and deployed in its early phases. This applies to the very first commercial deployment, but very likely the first several.

That leads to the canonical challenge in climate tech innovation - where does the capital come from to pay for the deployment of the first projects of any new climate tech - and likely the first N projects, where N is subjective but is where you get to true “bankability” and get to traditional project finance.

There are nuances to the problem

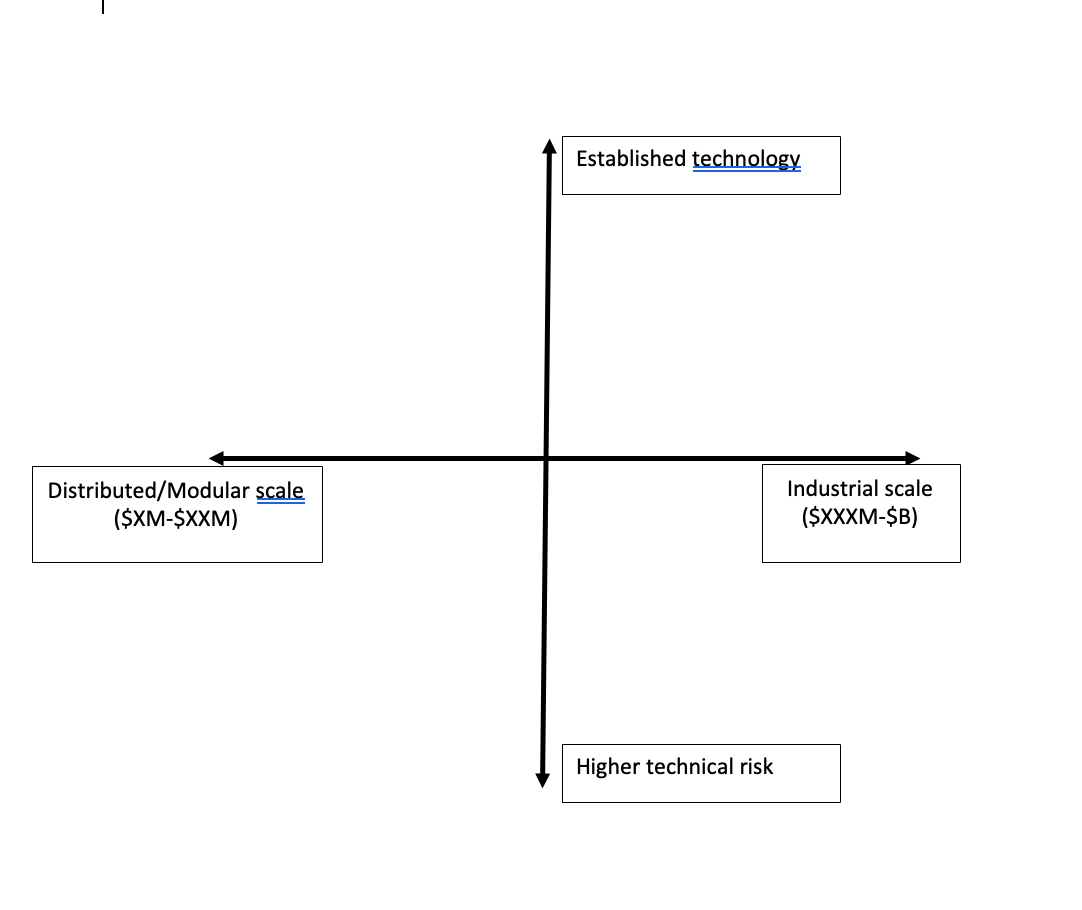

One of the challenges I see: there are nuances to the problem, and actually different categories of the problem within the “FOAK capital gap” category. It is not sufficient or helpful to talk about it as one broad problem. There are some technologies and projects that are increasingly more modular or more distributed, and have various levels of technical risk, and these struggle to get deployed because typical project finance and project development capital is not participating in this space because it is not incentivized to write smaller checks, often for the same amount of diligence. (There are some groups that have been doing a lot of good work in these spaces - see list below).

There are also technologies and industries where there are innovative solutions that will need to be at the industrial scale ($B sized project), but will have technical risk at the project size as it will inherently be the first time(s) they are being executed at that scale. A simple way to think about it is just that the problems fall in the following spectrum of scenarios (ignore the pathetic excuse for a graphic):

There has been a lot of good work and new experiments being tried in this general space. I’ve been keeping an eye on various initiatives that have been stood up focused on tackling different pieces or aspects of this problem. A table sits below of the approaches I’ve kept track of.

However, I don’t think most of these solutions are focused on the problem that Im focused on - the quadrant of being fundamentally new and therefore have some technical risk, and are also at industrial scale projects (let’s say, $500M-$B).

The Opportunity

That leads me to wonder - what would a new type of capital structure that is purpose built for this function look like? Ideally, one that is replicable and scalable, rather than a one-off fund. In my thinking about the issue, it is easy to think about it as a problem, but the more time I do, it seems like the need presents a very large opportunity. The way I break it down in my head is the following:

The scope is huge.

Estimates from McKinsey and BloombergNEF suggest that to reach net-zero, the world must invest an additional $3.5 to $5 trillion per year through 2050 on what is already spent, totaling from $7-$9.1T/year. That means: About $200-275 trillion of cumulative spending on physical assets would be needed over the next three decades under the NGFS Net Zero 2050 scenario [McKinsey, BNEF]

That is the biggest industrial transformation in history.

And what that industrial transformation needs is fundamental new technologies and innovation across industries that include the following:

Power : fusion, SMR, hydrogen, storage, geothermal,

Industrial: cement, steel, plastics, fuels, chemicals, textiles, mining

Agriculture: fertilizer & pesticide production, water / wastewater, alternative food production (proteins),

Transportation: batteries, auto, shipping, trucking, maritime

Other: carbon capture, waste to value, carbon utilization

And where is it today?

We can argue about what exact % of innovation is needed vs. what technologies already exist today to meet true decarbonization, but the answer is universally that we don’t have all the tech we need today. According to IEA, almost 35% of cumulative emissions reductions will come from technologies that are currently at the prototype or demonstration phase and that will need further R&D and technical development to become available at scale.

That means that there are several trillions that will need to be put to work at scale in things that are on the path of innovation to market right now, currently living in labs, prototypes, and early stage startups.

The nature of this problem is also that it has some latency. There has been an astounding amount of activity and progress in the climate tech ecosystem over the last 5 years. Since 2018, there has been a significant growth in capital at the early stage for sustainability in private markets, with over 30 new climate-dedicated funds and ~$50T of committed ESG capital. The Inflation Reduction Act ($369B) in the US, and the Green Deal Industrial Plan $270B (EU), have also changed the game from risk to opportunity. That means there is an accumulating set of companies developing technologies that are required for decarbonization that have not yet reached this stage.

A new asset class?

It seems as though that the combination of both the ticking clock on the climate crises and needing to deploy as soon as possible, paired with the fact that there is a crop of climate tech startups that are larger than ever before and will be progressing over the years, the need for this capital will only get larger, and the problem will only be getting more acute.

That scale, then multiplying it globally, has made me wonder what would the attributes need to be for a capital structure that would be a win-win that unlocks the deployment of critical technologies for climate, while also having the proper returns and benefits for taking the risk at this scale. And how to flip it from a burden to an opportunity.

What would that look like?

I’m still early in my thinking on this, but attributes would look like the following:

Some kind of blended capital between equity in the asset(s) and corporate equity, or maybe purely corporate equity that is okay with the stage and use of money. (It’s my opinion that most “growth” equity capital is either not substantial enough in amount of capital or would not be excited about the capital being put towards a project, rather than investing in the corporate capabilities.

It needs to have more upside than traditional project equity investors, given the amount of risk taken, but likely less upside than traditional venture/growth equity, which is typically taking larger risk earlier in the company life and risks on product, market, etc.

Maybe it has some sort of preference or ROFR to future plants or facilities, as a benefit or upside to taking the risk?

Maybe some sort of preference to the revenue that comes from these first projects (knowing that they won’t be as economic, but that these investors get the top of the stack for those revenues?)

Who are the potential types of investors?

LPs could potentially be:

The large multi-asset funds that invest across a variety of types, that do traditional project or asset finance, hold real estate, energy assets, etc.

infrastructure funds that are looking out on the horizon for the next pipeline of types of projects they will invest in.

energy companies - strategics - maybe O&G, who have large swaths of cash right now, but want to see the winners up front execute projects and help understand how these potential things could be used in their own operations or where there are adjacencies in their competencies where they see new business units or revenue streams

owners and investors of infras assets with mandates to decarbonize, with portfolios of stranded assets or brownfield sites - think pensions, sovereigns, endowments.

Note, the team that works here needs to serve as a language bridge - a group of folks who can translate between “VC/innovation/revolution” to “evolutionary/commercial debt/project finance” types.

For the right types, I feel like this could potentially be high leverage and there could be significant value capture:

Like the Rivian / Amazon deal, there is some element of investing in the first projects that “make” the company by doing the projects, increasing the value of the company, and increasing the value of the corporate equity that the fund itself would hold

Access to deal flow for LP’s other business lines

Acquiring the sites - land leases, maybe even changing amortization on their books for brownfield or stranded assets

Financing factories and other company build outs - get the loan payouts

Other lending and leasing vehicles

Access to deal flow early. There will be a time when these innovations are scarce - before they have fully matured and hit high scale - and there will likely be many players fighting for access or to get in line for access.

A head start to competitors - there will be lots of learnings on how to diligence and underwrite these projects, as no one has done this before, so there is an opportunity to get a leg up in knowing even how to evaluate them and structure deals in the future.

Becoming the go-to relationship. These companies are building capabilities and will lean on expertise and warm intros for who is in their network first - LPs can become the first calls for deals for new factories, new plants, sites for redevelopment, etc.

What are the challenges or what questions am I thinking about?

This is a lot of capital - it’s harder to experiment and try this out on the small scale for these sized projects, and then when you add in a portfolio, it increasingly gets large.

Perhaps the biggest question - I’m still not clear on what the right structure of the investment is and what a necessary and realistic return should be. And given that, how many investmentes in a portfolio do you need to have to distribute the risk?

Obviously, finding a way to thread the needle between appropriate returns for the risk being taken is the big challenge. Are some of the other benefits or value to LPs make this more interesting or willing to take on the risk?

How does the IRA, Green Deal Industrial Plan, and other government incentives and initiatives effect this? I think it is synergistic - still need equity holders in the projects even with tax credits and production credits - it just makes the economics of these early projects better and less risky.

Would factories make sense to put in here if they are new-age or new tech factories? Or does that not make sense to mix with other assets like chemical plants or power plants?

Are there enough companies? I think so but need to do the math.

I know I’m not the only person out there thinking about this. This is just a space for me to try to get what’s in my head down on paper, and to try to draw it out in a little bit more structured of thoughts. I’d love to connect with people on this and if you have any feedback, comments, ideas, or corrections of where I’ve got something wrong - I’d love to hear from you.